In this paper, the author deeply analyzes the development status of bean and fruit food and kitchen as competing products, and gives his own suggestions and prospects in combination with the development of domestic and foreign industries. Worth reading!

Experience environment:

- Mobile phone: Android 6.0.1 MI 4

- Bean and fruit food: Android v6.2.4.2

- Going to the kitchen: Android v5.9.11

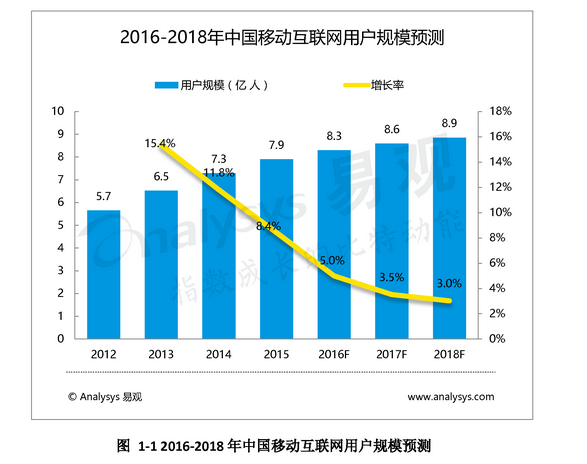

According to Analysys data, it is estimated that the number of users in cmnet will reach 830 million in 2016, an increase of 0.5% compared with 2015. It is estimated that in 2018, the number of users in cmnet will be around 890 million. The scale of users in cmnet will continue to expand.

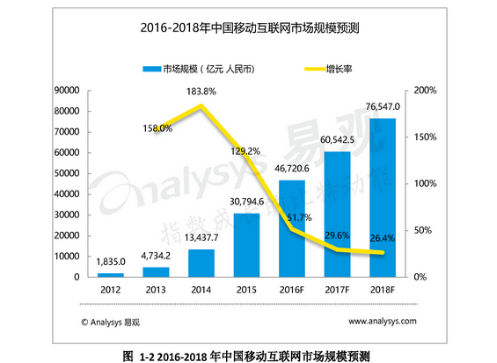

The huge market makes many enterprises from different industries, traditional or innovative, flood into the mobile Internet market.

As the "food" in the "basic necessities of life", it can be said that it is an indispensable part of people’s daily life, that is, it belongs to high-frequency demand. The catering industry is also expanding the boundaries of the Internet according to the needs of users.

In such a mobile internet era, the distance between users and food is shortened by selling, fresh food, recipes and other forms. The way of eating is gradually changing from simplicity to quality. Whether it is take-out or cooking at home, users gradually begin to pay attention to food quality and health.

Of course, there are also some innovative ways, such as catering O2O, inviting chefs to cook at home, socializing in catering, and making like-minded friends through table sharing.

If take-out is a passive choice in work or study life without too much time, then gourmet recipes must be the best choice for people who pursue quality of life in their spare time.

"Tip Tip 2" has once again set off a storm of food in China, and catering stores all over the country have also followed the dishes recommended by "Tip Tip 2", which is a good time to cut into the gourmet cookbook APP.

The mix of fish and eyes in the take-away market and the food safety of physical catering have always been our concerns. Although the take-away market has begun to rectify illegal operators, the video security problems in the physical catering industry are also being intensified, but there is still a long way to go from the healthy goal of the industry. More and more young people entering the workplace are willing to spend some time to choose a healthy diet, and they are more willing to choose to return to the kitchen.

Judging from the 24-hour active user period in the figure below, whether on weekdays or weekends, users are more active during lunch and dinner, especially from 11: 00 to 12: 00. Generally speaking, users’ habits of selling recipe apps are concentrated about half an hour before lunch and dinner, and the per capita use time is relatively concentrated.

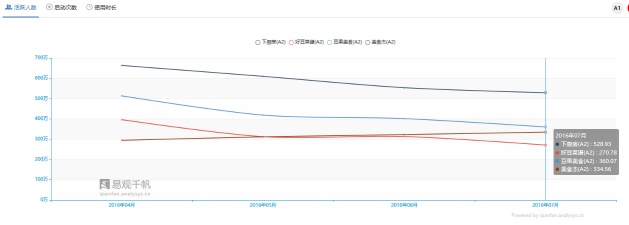

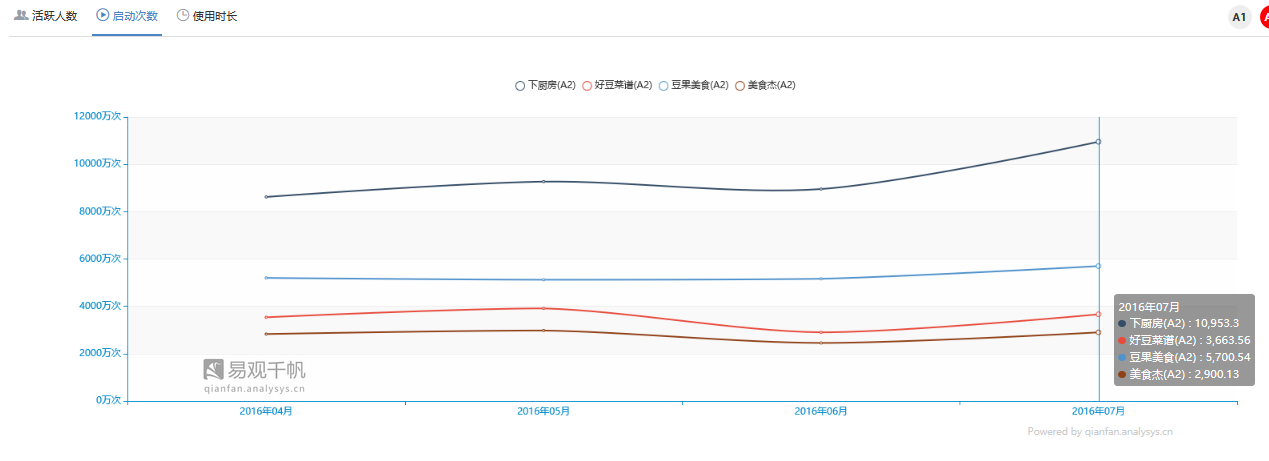

However, according to the data of Qian Fan in the following figure, from April to July, 2016, the number of people living in the kitchen, bean and fruit food, good beans recipes and food heroes ranked first with obvious advantages. By July, bean and fruit food and food heroes were almost equal, while good beans recipes were slightly inferior. From the trend, the overall four applications are in a decline of 1 million to 2 million.

Judging from the number of starts, the number of starts of the kitchen has increased significantly. From April to July 2016, it increased by about 40 million, far ahead of the other three gourmet menu APPs. It can be seen that the user frequency of the kitchen app is still quite high, and it is in the growth stage.

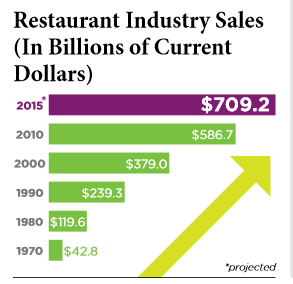

Take the United States as an example. According to the data released by the National Hotel Industry Association (NRA) in 2015, the total catering market in the United States is about 709.2 billion US dollars, accounting for about 4% of the total national economy of the United States, and the sales growth of the catering industry has never stopped in the past few decades, whether the economic situation is good or bad. Statistics also show that in the past 16 years (spanning two economic recessions), the employment growth rate of the catering industry has always outperformed the national economic growth.

Source of information:http://www.restaurant.org/Downloads/PDFs/News-Research/research/Factbook2015_LetterSize-FINAL.pdf

In a survey conducted by several companies specializing in developing mobile applications for recipes, it was found that one quarter of iPhone/iPad users in countries where English is used prefer to cook by themselves. In addition, according to the statistics of the National Hotel Association of the United States, 79% of diners say that high technology makes it more convenient to eat out, 70% of diners with smart phones will use the restaurant/menu application several times on their mobile phones, among which 34% of diners say that high technology makes them buy takeout or go to restaurants more often, while 32% of diners with smart phones prefer to use mobile applications instead of traditional ways to pay the bill.

The popularity of the application market is unprecedented. As of 2015, the total revenue of global applications is $41.1 billion, and it is estimated that the annual application revenue will be $77 billion in 2017. The following is an overview of the application market:

Source of information:http://www.startup-buzz.com/cooking-apps-revolutionizing-cooking-industry/

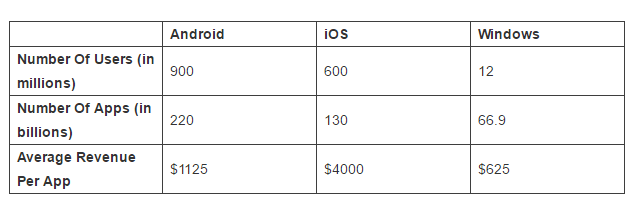

According to the above table, Android has the largest number of users, with 900 million. There are 220 billion APPlications in the Android application market, and the average income of each app is $1,125. Compared with the average income of the iOS version of the application, it may be related to the fact that the economic conditions of the user base of iOS are mostly better than the user base of Android phones, and the pricing of iOS applications is generally higher than that of Android applications.

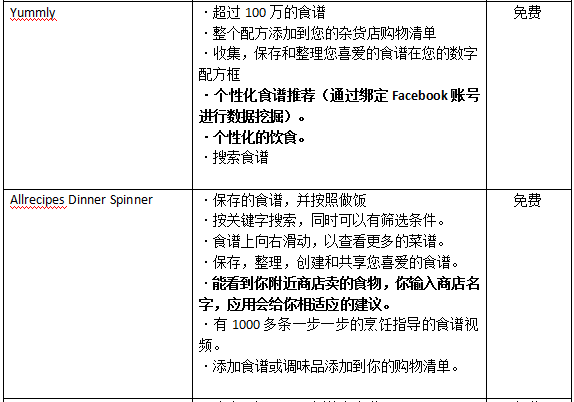

Based on the application recommendation and product evaluation of foreign catering recipes, the following five applications are generally recommended:

Source of information:http://www.startup-buzz.com/cooking-apps-revolutionizing-cooking-industry/

In addition, there are some different innovations in the catering recipe market abroad, such as Blue Apron, a company in new york in 2012, which provides fresh ingredients and corresponding recipes to be delivered to your door. In the food delivery business, you can customize different services on the website: meals for two people, at $59.94 per week, delivered three times, that is, three meals can be managed; Family meal, $69.92 or $139.84 per week, with food for 4 people delivered twice or four times each time. If you only provide ingredients, the price is actually not cheap, but you will be accompanied by recipes when you deliver them, so that you can learn the cooking methods of many chefs. It is quite warm to cook with your family at home.

In addition, compared with the domestic public comment, the ChefFeed is different from the public comment. It is an application platform that only chefs can recommend food, and it deeply connects the surrounding food and catering culture.

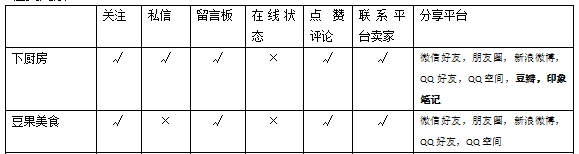

Judging from the data of four products in the domestic market, whether it is the monthly activity or the number of start-ups, the lower kitchen and Douguo cuisine belong to the first echelon, which is higher than the gourmet and the good bean recipe, while all the data of the lower kitchen are higher than Douguo cuisine, so it is determined that the lower kitchen is the competitive product of Douguo cuisine for further analysis.

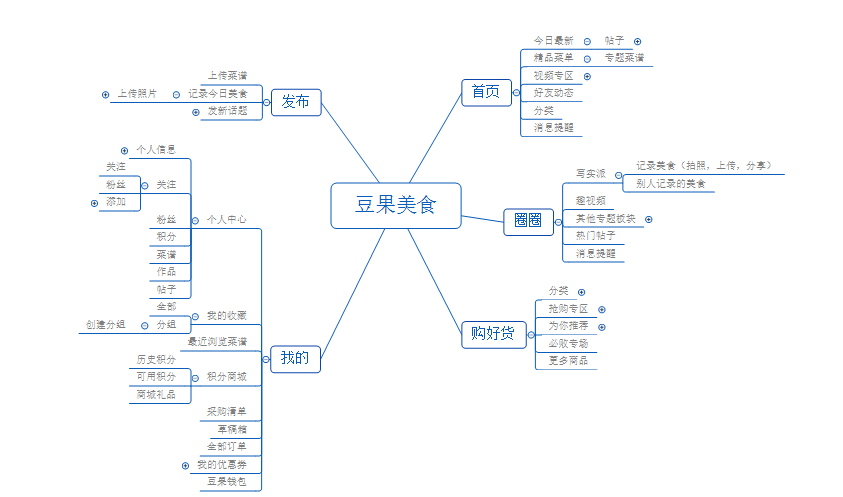

1. Bean and fruit food

(1) History of Douguo Gourmet Version (version above 0)

- 6.2.0.8:Upload recipes, upload food, upload posts together, and put them in an obvious position, which is more convenient to publish; Online menu barrage, you can participate in the discussion; You can join the circle to browse your favorite posts and record food. What is added is the fart circle, which is updated every day. Activity reminder.

- 6.1.8.2:The login system is optimized and the identity verification is convenient; The bottom of the product page can directly enter the store.

- 6.1.6.4:Recipe search supports ingredient combination search; Leave the menu editing interface without saving, and give a reminder.

- 6.1.1.2:You can add associated friends.

- 6.1.0.2:There is an entrance to view the encyclopedia of ingredients in the menu.

- 6.0.7.2:Gourmet experts and quality shops can share them with friends.

- 6.0.6.2:Menu classification adjustment.

- 6.0.5.2:Personal center supports sharing to third-party platforms.

- 6.0.4.6:Optimize the uploaded pictures and adjust the page layout.

- 6.0.3.8:Show food channel: hot topics, increase rankings, and popular users.

Judging from the iteration of the version of Douguo Cuisine, from version 5, Douguo Cuisine focuses on the function and interface iteration of e-commerce nodes. Compared with the iterative efforts of e-commerce, Douguo cuisine has also made some adjustments in social elements, all of which are public messages and concerns, without further social means such as private letters. Therefore, the development direction of bean and fruit food is more inclined to e-commerce.

In June of this year, the bean and fruit food made a sound, and proposed that the future development direction should focus on kitchen smart appliances and cooperate with hardware manufacturers to provide users with intelligent overall kitchen solutions; And rely on huge user data to provide food big data for enterprises.

Imagine the smart kitchen carefully. For those who can’t cook and don’t have time to learn how to cook, they can also enjoy the fun of cooking by themselves. This undoubtedly magnifies the target user group of the platform for many times, from food experts to lovers who are interested in cooking and have time to zero-based food lovers who are only interested in eating.

We can also imagine such a scene. Xiaobai users open the APP to find the recipe they want to make, and purchase semi-finished ingredients with one click through the link provided by the recipe, so that only kitchen utensils can be connected with the favorite recipes in the bean and fruit APP, and the kitchen utensils will remind users according to the data. For example, when refueling is added to a certain time, the control panel of kitchen utensils will remind the user that it is OK. For example, the process of putting what materials first and then putting what materials, such as big fire first and then small fire, is controlled by only kitchen utensils.

However, if you want to connect with kitchen utensils, the data requirements for recipes are relatively high. In the early stage, after encouraging users to output high-quality content, you can consider joining the audit mechanism. If the audit meets the requirements, you can mark "Support for smart kitchen utensils", so Xiaobai doesn’t have to worry that his cooking will be affected by inaccurate data.

As far as the current semi-finished market of bean and fruit food is concerned, it focuses on fast food, dry ingredients and other ingredients whose shelf life is not so short, rather than fresh processed ingredients, which does not meet our daily needs for three meals, and the one-click purchase of ingredients in the recipe is actually delivered by different merchants. Therefore, there is also a gap in the time received. Even if you buy more dishes at a time, you have to go back and spend time combining them. You can consider adding some usage scenarios, such as recommending recipes and ingredients for one week according to the data of recipes that users usually browse and collect, filtering the number of people, the meal time, what taboos are there, etc. One-click purchase of recommended recipes can be packaged according to recipes, saving users’ sorting time.

(2) The development history of bean and fruit food.

- In January 2008, Douguo Cuisine was established, which belongs to Beijing Douguo Information Technology Co., Ltd., and its CEO is Wang Yuxiang.

- In 2011, bean fruit net received a venture capital investment of RMB 10 million from Shanda, and bean fruit net began to be formally commercialized.

- In January, 2012, it became the best application of the only flat cabinet AppStore in China.

- In 2012, bean fruit net received a series B financing of $8 million from ggv capital (GGV).

- In 2012, the mobile phone client of food diary was officially launched in public beta, and now it is renamed as "Writing Food School".

- In 2013, it won the third round of financing from Gaochun Capital and Qingliu Capital, and the company was valued at 120 million US dollars, making it the largest gourmet community in China.

- In 2013, we began to test water e-commerce and cooperate with SF Express.

- In 2014, the first "Douguo 2013 China Annual Food Festival" was held.

- In 2014, Douguo became the official exclusive online communication experience community in the second season of China on the Tip of the Tongue.

- In November, 2014, we completed the $25 million Series C financing.

- In 2015, it was ranked in Baidu Mobile’s "Top Ten Popular Applications List of the Year" and won the "Life Application Award of the Year".

- In 2015, it entered the field of semi-finished food, adding a new business model for fresh e-commerce.

- In 2016, the "Bean and Fruit Food Festival" was opened, and the latest version of "2015 China Food Network Development and Trend Report" was released.

- In 2016, Douguo Cuisine joined hands with Boss Electric to build an intelligent cooking ecosystem.

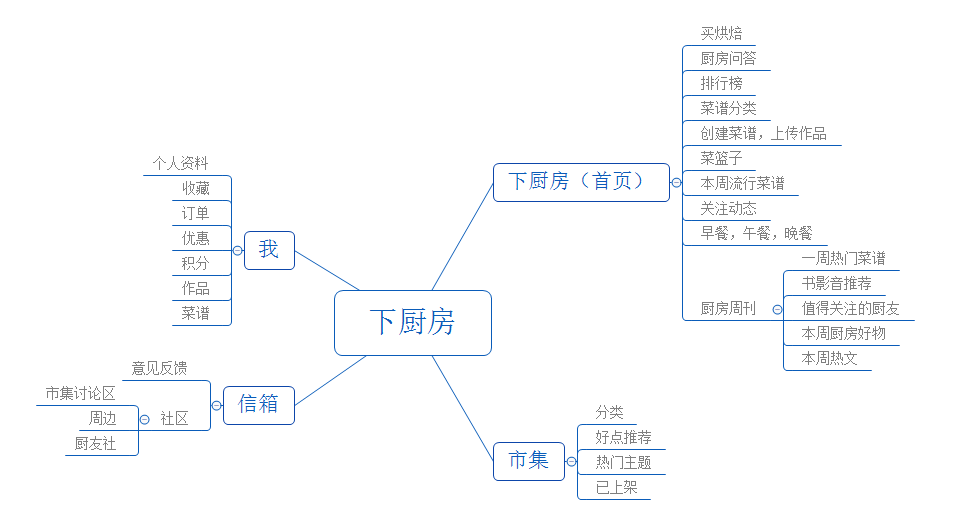

2. Go to the kitchen

(1) the kitchen version history

- 5.9.8: personal homepage and homepage upgrade; New icon design to optimize visual effects; Optimize the collection of menu pages and the location of menu buttons; Market goods can be paid by points when placing an order.

- 5.8.3: You can upload works and recipes on your home page; Message revision of the menu: the ordering process is optimized, so you can buy it in buy buy better.

- 5.5.6The list of conversations in the mailbox can be deleted, and the conversations you don’t want to see are out of sight, out of mind; Share recipes to WeChat or Weibo, and you will find that sharing a copy knows your heart better; We understand that the word limit for market commodity reviews has been abolished.

- 5.5: Add instant messaging function to facilitate communication between kitchen friends. You can also communicate and consult directly with merchants when shopping in the market; Menu browsing has a big picture mode, clearer menu pictures and more friendly interaction, which will help you become a better chef; Fixed such and such bugs.

- 5.4: Now the function of creating recipes on mobile phones is more perfect, adding exclusive logos and recommending them to categories; It is found that personal profile and pictures of TA’s works have been added in the friends module; Provide relevant suggestions when searching to make your search more efficient; The market increases the choice of regional positioning.

- 5.2.2: Increase the payment method of WeChat; Optimize the home page search menu; Product recommendation is added to the product details page; Show the description of the work in the message reminder; The menu message type in the message reminder can directly jump to the menu; Optimize video playback.

- 5.2.0The merchant can explain the commodity evaluation; Commodity evaluation adds useful and user message function; Commodity evaluation can be synchronized to the personal homepage and pay attention to the dynamics; The personal homepage has added the buy buy Buy module; The shopping cart adds a drop-down refresh function; Community posting forces the binding of mobile phone numbers; Optimize the product evaluation pictures shared to the circle of friends; Optimize the logic of sharing to WeChat to prevent sharing failure.

- 5.1.0: Revision of the product details page-adding graphic details-giving priority to the evaluation of blueprints-the evaluation list is displayed according to blueprints/all categories; Increase the function of searching for goods in the store; Home page [buy buy Buy] page optimization; Topic optimization of breakfast, lunch and dinner.

From the iteration of the version of the kitchen, we can see that from the version 4, the kitchen began to add social elements, such as the sharing function in the market, the personal homepage to find friends, the positioning function in the market, and the interaction with the surrounding kitchen friends. The increase of these functions seems to pave the way for LBS-based socialization. No matter how active online, gathering fans offline and making strangers have a weak relationship with food as a clue is a good means to maintain users in products for a long time.

Including some time ago, the kitchen was doing a little field, and building a platform and introducing a farm was an attempt to realize the commercialization of the kitchen, all of which reflected the kitchen’s efforts to make ordinary users (non-deep users) participate in offline activities or social activities as much as possible, and take the kitchen as a platform to retain these users and increase their stickiness.

Based on this, I think of Xiaomi’s core marketing concept "sense of participation", which uses forums to precipitate users, and uses humanized and comprehensive customer service, online and offline activities of rice noodles, including the annual rice noodle festival, to gather users and spread word of mouth.

Then why do you want to do LBS in the kitchen? After consulting the recent news, the author thinks that the original intention of doing LBS in the kitchen should be to eat friends, but because the specific operation plan is not clear, the community of "peripheral" nodes is hidden in the "mailbox" where it is not easy to notice. Therefore, the LBS in the kitchen is in the exploratory stage. How to operate and what is the development direction is still not very clear, and users may need to explore it.

(2) The development of the kitchen.

- In March, 2011, the kitchen website was put into operation, and it was affiliated to Beijing Ruidi Interactive Technology Co., Ltd., and its founder was Wang Xusheng.

- In July 2011, the kitchen APP was released.

- In June 2012, it was invested by Angel Bay and Jiuhe Venture Capital.

- In October, 2012, it won a multi-million-dollar Series A investment from Lianchuang Ceyuan and Zhixin Capital.

- In November 2014, the "market" was launched and e-commerce operations began. It has been successfully transformed from a cookbook tool application to a family food portal that integrates the attributes of tools, community and platform e-commerce.

- In July, 2015, it was announced that it had completed the second round of financing of US$ 30 million, which was led by Huachuang Capital and JD.COM, followed by Zhixin Capital and Lianchuang Ceyuan.

- On December 1, 2015, Yiguo Fresh announced that it had reached an exclusive cooperation with the well-known domestic online family food diversion entrance "Xiachu".

- In 2016, the kitchen became the first entrance to family cuisine.

The product attributes of Douguo cuisine tend to be "community+e-commerce". Taking advantage of having accurate users of food and introducing e-commerce platform, Douguo prefers to cooperate with high-end platforms and pay attention to socialization.

The kitchen is a product that integrates tools, communities and e-commerce. Mainly meet the needs of users in four categories:

- Inquire about food practices;

- Share food practices and food works;

- Communicate around food;

- Buy ingredients, kitchen utensils and other items.

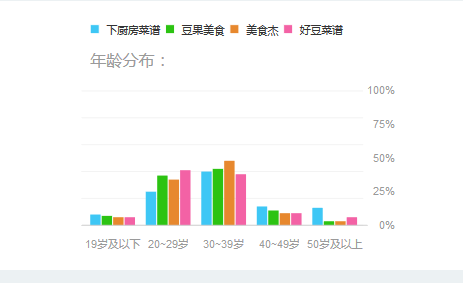

sex distribution

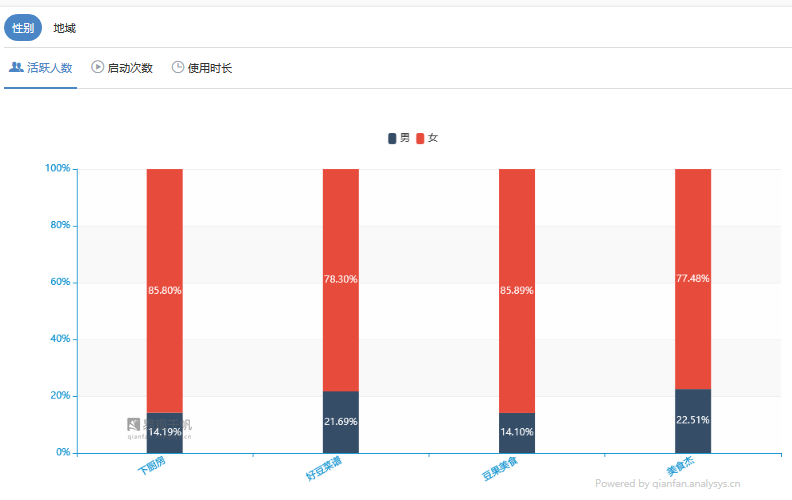

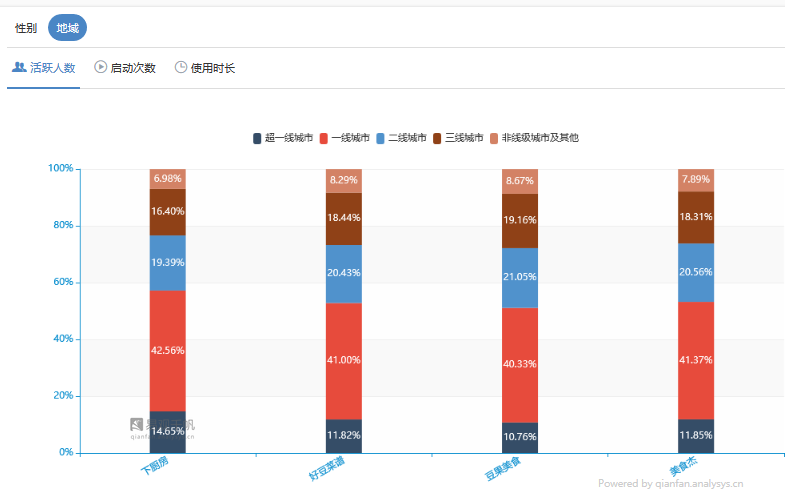

As can be seen from the following figure, in terms of gender, more than 75% of the users of the four products are women; Geographically, more than 50% of the users of the four products are in super-first-tier cities or first-tier cities; In terms of age, the users of the four products are concentrated in the age of 20-39. It can be inferred that the target users of the application are white-collar workers or housewives aged 25-35, who have the leading role in the kitchen economy, have certain consumption power in first-tier or super-first-tier cities, pay attention to the quality of life, and are good at using cookbook apps.

A kind of user portrait:

White collar Xiaomei

- Local, born in Beijing, from a prestigious school, working in a listed company, working in a high-end office building, working in a super-first-tier city, with a busy job.

- Just married, pay attention to the quality of life, pay attention to food quality;

- Dining habits: I usually eat in the company at noon, go home to cook with my family at night, and sometimes show off with my parents on weekends.

- Features: Pursuing quality of life, preferring high-end fresh and healthy ingredients.

Two types of user portraits:

White collar Xiaoer

- Graduated from an ordinary domestic university, born in a third-tier city, working in a small and medium-sized enterprise in a first-tier city, renting a house.

- Single, often take food to the company to eat, will pick some Aauto Quicker food to learn.

- There are many friends who usually have dinner with roommates or friends after work or on weekends, and usually choose everyone to cook to show their cooking skills.

- Characteristics: undergraduate, in the struggle period, with low annual salary and pragmatism.

For a class of users, discounts and promotions are the second, and you need to buy fresh food, or you will click on the commonly used dishes APP to cook when you see the dishes you want to learn. Offline cooking learning activities, healthy diet recipes and knowledge popularization are more important.

For the second category of users, concessions, subsidies and promotional activities are all important indicators, and more attention should be paid to such users for event reminders and pre-sale reminders.

geographical distribution

age distribution

Social elements

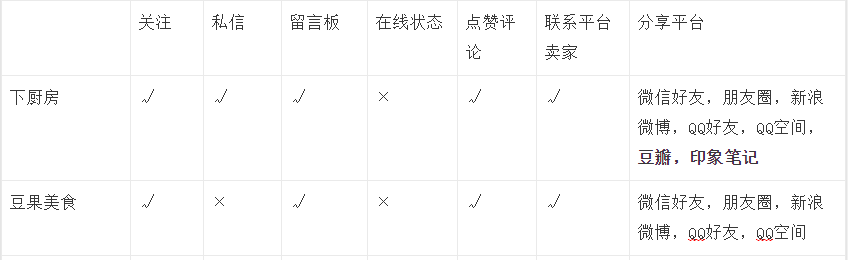

(1) Bean and fruit food

Bean and Fruit Gourmet APP (Android) 6.2.4.2 Version Function Module

The navigation bar at the bottom of bean and fruit food is home page, circle, release, buy good goods and my five modules respectively. The home page is the page of the menu, and the circle module belongs to the social module. You can join various circles, view posts and interact with the landlord’s comments. Buying good goods belongs to the e-commerce module, and the combination of scenes and posts makes the advertisement and the advertisement of goods feel no contradiction, while mine is the user’s personal information.

(2) Go to the kitchen

The navigation bar at the bottom of the kitchen is divided into four modules: kitchen, market, mailbox and me. The kitchen is the home menu module, the market is the e-commerce module, the mailbox is the community communication module, and I am the user personal information module.

Both of them are designed based on the framework of home page-mall-community-individual, and their logical structures are relatively clear.

On the framework, it is worth noting the following points:

- There is LBS positioning in the kitchen, so you can recommend products according to the positioning, and there is an entrance on the home page, so you don’t need to switch the bottom navigation.

- There is a kitchen question-and-answer category on the front page of the kitchen, which contains questions about cooking skills and food preservation. The questions are very practical and are encountered in life, but they may not be mentioned in the menu to make up for the vacancy of cooking details. At the same time, it can increase the interaction between users and enhance the activity of the community.

- You can go to the kitchen to @ Chuyouyou, and the Chuyouyou community can go offline.

- LBS positioning in the kitchen can see the people and distance around you and interact with the people around you.

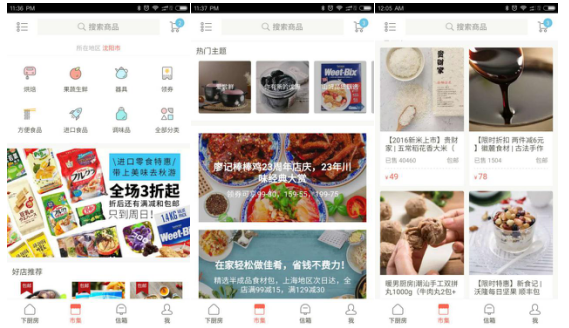

(1) Startup page

After downloading the application, it was launched for the first time. The initial launch pages of the two apps are all in a small and fresh style of literature and art. The bean and fruit food is in a white background, and the kitchen is in a style of delicacies and masks, which are in line with the overall positioning of such applications. When the bean and fruit food and the kitchen are started again, there will be advertisements on the startup page. The advertisement for going to the kitchen is a discount advertisement for snacks of e-commerce in its own application. Douguo cuisine is a free activity advertisement promoted in cooperation with electrical appliances merchants. At the same time, Douguo cuisine also has a pop-up advertisement similar to the menu competition when it enters the theme interface.

(2) Menu Home Page

From the home page, you need to pay attention to the following points:

1) user operation process

Douguo Cuisine puts the release (recipes, posts and recorded food) in an obvious position in navigation, and others’ recipes are displayed in the form of floating windows, which is higher than the bottom display in the kitchen, so Douguo Cuisine is generally more inclined to let users publish more topics. However, it is not obvious that the kitchen puts publishing and creating recipes in the upper left corner. The kitchen pays attention to buying raw materials and then learning to do it. Seeing recipes-collecting raw materials-buying raw materials-cooking, uploading-sharing, the process is complete.

2) On the main interface classification

Today’s latest, boutique menu and video zone in bean and fruit cuisine are actually recipes. We can consider merging today’s latest and boutique menus into one entrance and then diverting them. For the kitchen, the four categories in the main interface are all drainage processes. In order to drain the e-commerce, the chef’s question and answer is to supplement the lack of recipes. The leaderboard is slightly duplicated with the following popular recipes this week. The leaderboard is a boutique menu with edited attributes, including video recipes.

3) Using the scene

The kitchen is divided into three scenes: breakfast, lunch and dinner in the middle of the home page. After opening, it is the work uploaded by the user, and there are links to the corresponding recipes. At this point, you can like to comment on the kitchen friends, and you can try the recipes. User works and recipes form a closed loop.

4) Material purchase

When going to the kitchen, it is considered that users sometimes want to cook a dish, but they don’t want to buy it for the time being. For example, they want to go home and see what ingredients and seasonings are missing before buying it. At this time, they can use the shopping basket to prevent the shopping cart from being messy. The shopping basket is classified according to the recipe. But on the other hand, this undoubtedly adds one more link to the process from reading recipes to buying, and may also lose users in this link. Users can consider adding if they need it.

(3) Classification navigation comparison

The top row is the classification of bean and fruit food, and the bottom row is the classification of the kitchen.

Judging from the practicality of the whole secondary menu, the simpler the menu, the less depth it has, and the easier it is for users to accept. For example, the kitchen belongs to the classification interface menu, which can be seen without clicking on the popular classification. You can see the menu with more views by clicking on a classification at will, and you can reach the classified menu in one step without the need for users to select it many times. But it is not very clear how the recommended menu crosses many choices and enters my field of vision. If beans and fruits can be combined to make users achieve the ultimate goal of recipes with as few operations as possible, plus the current screening of classified recipes (the best comprehensive, the most collected and the most done), it will be excellent.

From the classification icon, the classification icon of bean and fruit food is in the upper left corner, and you can’t see what this icon is for at a glance. Maybe bean and fruit food is more inclined to let users search for keywords themselves; Go to the kitchen and put the menu classification in the obvious position on the home page, giving users who have no idea a direct entrance choice.

From the use of the scene, the kitchen to join the dormitory, banquet, picnic and other scenes. Considering the poor cooking materials of the student party in the dormitory, it is also a large number of users. Bean and fruit food also has scenes such as two-person world and moon meal, but it doesn’t seem to be so intuitive.

(4) E-commerce

1) the whole

The top line of the above picture is the e-commerce interface of bean and fruit food, and the bottom line is the e-commerce interface of the kitchen.

From the layout of the interface, they are all up and down, and all the elements are classification, recommendation (store or commodity), theme or special show, and the above the fold interface has advertisements for its main products. The advertising area in the kitchen is too large.

The search function of bean and fruit food is repetitive, and the jump interface is the same after operation. I feel that it is enough to leave one in the upper right corner and the upper middle of the screen.

From the way of classification, it seems similar, but it has different emphasis. The secondary menu of bean and fruit food is a little small, so it is not easy to choose accurately. The classification of bean and fruit food includes semi-finished products, grain and oil seasoning, baked chefs, snack foods, selected fresh foods, imported foods, drinks and tea, kitchen appliances and many other categories. Among them, the semi-finished products are placed in the first place in the classification label, which is enough to show that the bean and fruit food attaches importance to the sales of semi-finished products. The market in the kitchen is divided into baking, fresh fruits and vegetables, utensils, convenience foods, imported foods, condiments and other categories, and the categories are also very complete. The kitchen also operates UGC’s gourmet products, aiming at small freshness and long tail.

From the product interface, the typesetting of the product description in the kitchen is more comfortable, the text is large, and there is a link to introduce it. The author opened the label of convenience food at will, and even saw the rice noodles of Funiutang, and the story of Funiutang was also in it, which opened Mr. Snail Powder at will and increased his knowledge of Snail Powder. Sometimes it may be important to evaluate, but the introduction information of the product before buying is also a key factor to determine whether you are interested in this product. Bean and fruit food is similar to the goods and introduction of Taobao interface, focusing on the evaluation and authority of the store (authentic guarantee, direct supply of origin, after-sales guarantee, authoritative supervision and so on).

Regarding the payment method, Douguo Cuisine supports Alipay, WeChat, Apple Pay and UnionPay card. The kitchen supports Alipay and WeChat payment, and no other entrance has been opened.

It is worth noting that in personalized recommendation, Douguo Cuisine will recommend ingredients according to a person’s collected recipes, and will also recommend your promotional products (I don’t know if the order of promotional products is personalized). At this point, the kitchen is a way to recommend good shops and give users more choices.

In addition, among the hot topics in the kitchen, early adopters need members’ points, and members’ points need to buy products on the platform. There are points thresholds and rules, which stimulate the purchase desire of users who love early adopters on the platform and stimulate the operation of the entire e-commerce platform. Bean and fruit food is to use the countdown to snap up to lure impulsive users, which seems to be less creative than other e-commerce companies.

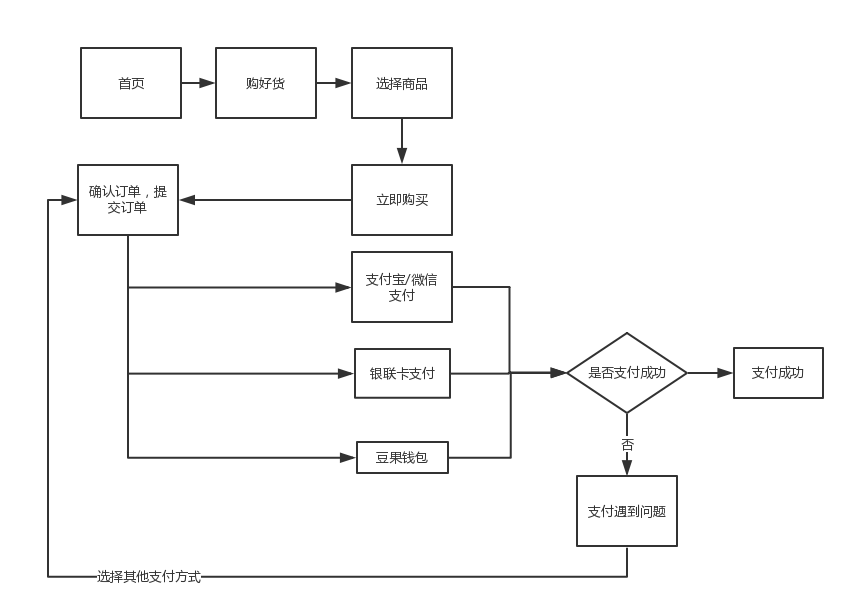

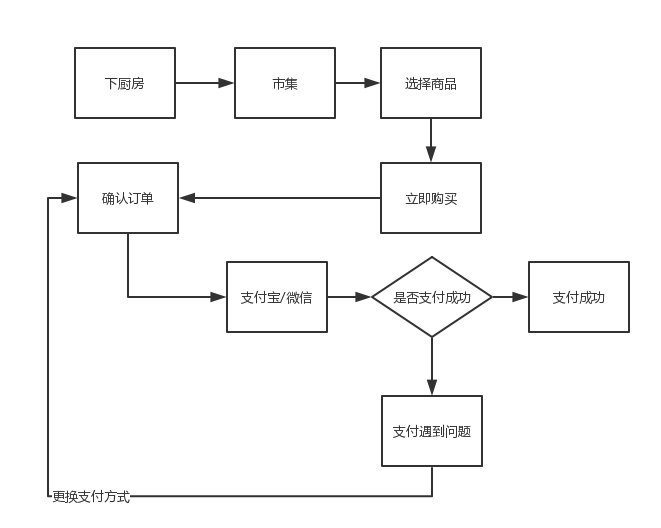

(5) Purchase process

Douguo gourmet

Xia kitchen

Compared with the kitchen, Douguo Cuisine now supports more payment methods. Besides Alipay and WeChat payment, it also supports UnionPay card payment (including credit card and savings card) and Douguo wallet. But at present, the bean and fruit wallet comes from the appreciation gained by uploading works. There are coupons for both products, but there are no coupons for the first order of Douguo Cuisine. New users in the kitchen will get two coupons to encourage them to place orders (but the deadline is three months, which is a bit long, and users will forget it).

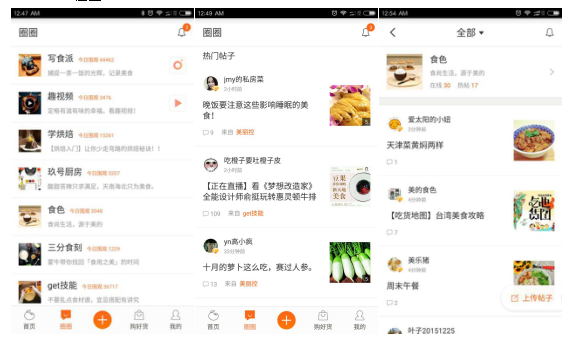

(6) community

Both the kitchen and the bean-and-fruit food are classified into communities. The above one is a community of bean-and-fruit food, which is called circle; The following is a community in the kitchen, called mailbox.

For bean and fruit food, you can choose to join the circle you are interested in, or read the post directly. Except for the first three circles, the names of the circles may not have such a strong purpose. Only by clicking in can you know what is written in them, usually the cooking and cooking stories written by users. You can comment or pay attention to a user, but there is no private message function, and the interaction is based on openness, so the sociality is not so strong.

For the kitchen, there is nothing in the mailbox without adding a kitchen friend, which plays the role of feedback. The surrounding area, market discussion area and offline kitchen friends’ club are hidden in the upper right corner, presumably in order to concentrate on communicating with kitchen friends instead of chatting in groups. However, the interaction between the users on the platform and the kitchen is enhanced.

Going to the kitchen guides offline interaction through positioning. Independent of the discussion group, it is speculated that it may be easier for the kitchen friends around to learn cooking offline, and encourage and facilitate the offline communication of users. Including the Kitchen Friends Society, it also guides online users to the offline. For Douguo cuisine, there are indeed some experience stores in some cities, but they have not yet become large-scale. Before they become large-scale, it is suggested to establish more offline activities to make fans from all over the world form a scale and promote the formation of offline experience stores.

(7) Login interface

1) Registration process

- Bean and fruit food: register → fill in the mobile phone number, get the verification code, fill in the verification code → fill in the nickname, set the password → enter the homepage.

- Go to the kitchen: register → fill in the mobile phone number, get the verification code → confirm the number and send a message → fill in the verification code, set the password → improve the nickname and avatar, and finish → enter the home page.

In terms of the number of overall process steps, there will be multiple steps of verification and confirmation in the kitchen, but there is no step of setting nicknames in the kitchen. After registration, they all go to the personal information interface. You can consider going to the home page to make a guide for users to use it for the first time.

2) Login process

The login process includes entering the mobile phone number/email address and password to log in. Both products support QQ, Sina Weibo third-party login, Douguo Cuisine supports WeChat login, and the kitchen supports Douban login, which is the difference between the two third-party login.

For accounts with third-party login mode, you can find the mobile phone number or email address, and there is no need to improve the mobile phone number or email address information.

For the account with wrong password, there is no hint of wrong password for Douguo Gourmet, but there is a hint of password mismatch in the kitchen.

Temporary login: the kitchen supports temporary login of SMS verification code, which is a bit cumbersome, but it does not support WeChat login for the time being, which is also a transitional way. It is suggested that temporary SMS login can be removed after supporting WeChat login.

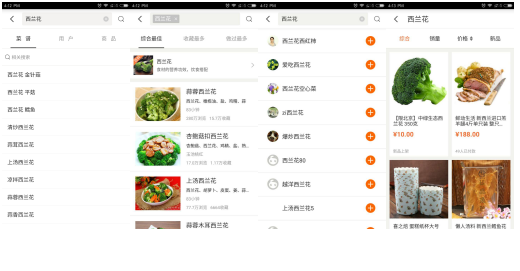

(8) Design comparison of food search function

In terms of classification and layout, the search of bean and fruit food is classified into three categories: menu, user and commodity. The default is menu, and there are three categories under the search box, which has a friendly interface. The kitchen is divided into three categories: recipes, kitchen friends and menus. The menus are uploaded by users, which have more social attributes than bean and fruit food, and bean and fruit food has more e-commerce attributes than the kitchen.

In the related search display, the bean and fruit food search broccoli got more related searches.

1. Accurate advertising

There are generally three positions for advertising in the kitchen: one is to start the interface. Recently, electrical appliances and snacks are more common, and their own platforms are operated, which is equivalent to advertising themselves; Second, it is placed on the lower side of the homepage of the recipe. At present, it is mainly the baking college competition and the soft text of milk powder. There may be soft text advertisements of e-commerce companies such as Tmall, and some activities belong to their own platforms; The third is the advertisement of ingredients or tools in the menu.

2. E-commerce sharing

(1) E-commerce commission mode of cooperation with C-side sellers

Different from e-commerce platforms such as Taobao, the market is the beginning of long-tail categories, which are short-boards sold on Taobao. Taobao’s comments on food are different from clothes, and users often can’t give detailed, vivid and rich comments, which makes it difficult for users to directly make purchase decisions on unfamiliar foods through comments. Therefore, Taobao’s decision-making system can’t well bear the long-tail food of the minority in the kitchen and housing market, which provides opportunities for the vertical product of the food community.

Most of the businesses in the city are consumers. What is more distinctive is that many businesses sell homemade food, coupled with a strong description of "literary style" and word-of-mouth publicity from the community, forming a unique vertical e-commerce for food products.

(2) Cooperate with B-side merchants

Earn traffic commission by cooperating with electrical appliances merchants; Promote the e-commerce of other big brands through some soft-text advertisements.

3. Peripheral consumer goods

The kitchen and the platform’s gourmet experts cooperate to publish food books, and earn commissions in the form of food writers and e-commerce.

1. Accurate advertising

There are generally three positions in the advertisement of bean and fruit food: one is the start page, and the pop-up advertisement on the home page after the start page, which is the activity advertisement of most cooperative businesses; Second, the advertisements of other well-known e-commerce companies in the home menu list (JD.COM, Tmall, etc.); The third is the advertisement of ingredients in the menu.

2. E-commerce sharing

There are B-end merchants and C-end merchants in the purchased goods. Similar to the kitchen, we earn commissions by cooperating with B-end merchants and earning platform profits by certifying C-end merchants.

3. offline experience store activities

By organizing experience activities offline, periodic activities will teach you how to make delicious dishes, create an offline fan economy, create a good reputation, and realize online diversion of offline activities.

4. Data output

By analyzing users’ behaviors and excavating the shopping habits of mainstream users, it is beneficial for kitchen appliances manufacturers to design products and for technology companies to monitor the indicators of health management software.

From the initial positioning point of view, Douguo Cuisine and Kitchen are both from the category of gourmet cookbooks, and they have similar basic functions of cookbooks, which is the basic condition for gathering users, making the user attributes of the two products somewhat homogeneous.

From the main business point of view, bean and fruit food and kitchen both include recipes, vertical e-commerce and social elements.

But from the menu function, the interactive experience of bean and fruit food is better. One-click purchase, comment barrage, learn to take photos and collect in the form of floating window, so that users can purchase, comment, transmit works and collect no matter where they go to the menu. The effect of hanging window is different from the display mode of bottom navigation, which is more in line with the display mode of secondary menu. However, there are many options for hanging windows, which are not centralized and easily distract users’ attention. We can consider reducing the options in hanging windows. It is suggested that only one-click purchase, comment and collection should be left, and comments should be placed at the end of the article. Only after learning to do this dish will there be a need to upload works. Therefore, it does not belong to the demand of high frequency, and it is more appropriate to put it at the end of the article.

Comparatively speaking, the interface font of the kitchen is relatively large. At the bottom of the menu are options similar to the navigation at the bottom of the home page, including collection, (one-click purchase), adding menus, and the lack of boundaries between options in interaction is not so smooth. The food basket and the menu are a little repetitive, and the menu is a little repetitive with the collection. The menu belongs to the collection, but there is an option of classification. It is suggested to simplify the hierarchical relationship of this part and classify the recipes in your collection.

From the perspective of business model, advertising revenue and e-commerce cooperation revenue are the similarities of their profits.

From slogan’s point of view, the "opening a delicious life" of bean and fruit food and the "only food and love can’t live up to it" in the kitchen are more literary and artistic, which is in line with the writing habits of young literary and artistic groups. Later propaganda can also start from the stories of food and love of such groups; Bean and fruit food is universal, simple and easy to understand, and can be accepted by food lovers of any age, but it is also easy to forget and exclusive.

From the development direction, the lower kitchen is biased towards social elements, and the bean and fruit cuisine is biased towards the construction of smart kitchens. At present, the kitchen has been able to interact with the surrounding kitchen friends based on LBS positioning, private messages, attention, and even check the other’s friends, offline dinners and other deep social factors, while the bean and fruit cuisine is still in the process of establishing a weak relationship and has not built deep social elements. The focus of bean and fruit food is to cooperate with kitchen appliance companies to build smart kitchens. The difference in strategic direction may make the target customers of the kitchen and the bean and fruit food different.

From the business model, bean and fruit foods tend to export big data, and cooperate with kitchen and electrical enterprises to form a new economy of smart kitchen. The core is to provide consumers with intelligent interactive experience, and beans and fruits provide content to promote brand marketing. The kitchen seems to cooperate with fresh e-commerce, and wants to improve the shortcomings of its fresh e-commerce in the supply chain and logistics providers. This also makes the two different. The cultivation of bean and fruit food for food eating white can start from the smart kitchen, attract a large number of peripheral users, go to the kitchen to deepen community users and improve the fresh e-commerce market.

1. Cut into the live broadcast platform to help social elements.

Learn from the live nom made by the founder of YouTube, take food as the theme, and decentralize it, so that every user has the opportunity to share his own food story (which may be related to travel), and can broadcast the process of making a certain food, enjoy the food, how to run a restaurant, or any story related to food. You can cooperate with the big names in the food industry, or with the stars who like to bask in food, so as to increase the entertainment and authority of the live broadcast. (nom)

2. Increase the search portal of mainstream social media and recommend more friends who love food.

At present, the bean and fruit food is in the format of sharing pictures, and the pictures are shared with other social media in the form of text and QR code, thus achieving the function of drainage. However, it may be more intuitive if we share our works on Douguo in the form of articles with an attractive title, and add the entrance to download and open the Douguo gourmet APP in the article.

In addition, from the perspective of content operators, at present, Douguo cuisine supports the menu in the form of video, but does not support sharing. You can consider sharing the intuitive and beautiful things (fine articles+fine videos) in the form of articles, which will have a great influence according to seasons and hot events.

3. Add scene elements

Some scenes can be designed according to the living conditions of users of some mainstream age groups to attract the user groups in this scene. For example, keywords such as dormitory, light meals at work and weekends are added to remind users that "Hey, even if you don’t have perfect kitchen utensils and environment, you still have the right to enjoy a gourmet life ~" "Hey, friend! Let’s cook a new dish at the weekend ~ "(Sorted)

If you have a healthy diet card, you can consider diverting users and operating a universally recognized organic field. This operation may be troublesome. If you think about it in the long run, you can first lay out the layout from the perspective of finding a partner.

Considering that the development direction of bean and fruit food tends to cooperate with kitchen electrical appliances enterprises to launch the life concept of smart kitchen, there should not be only fast food and dry goods for semi-finished modules, because it does not meet the requirements of ordinary users for three meals and the pursuit of nutrition. It is suggested to add some scenes, such as the recommendation of a basket of ingredients in the autumn essential weekly recipe, packaging semi-finished products according to the ingredients in the recipe, and trying to don’t make them think.

For the ingredients that need to be reprocessed by users, we can consider indicating the commonly used dishes and how to deal with them on the packaging, so as to provide sufficient food service for Xiaobai users. In this respect, we can consider cooperating with fresh logistics enterprises such as Shunfeng to build fast delivery of semi-finished products with fresh quality.

4. Add sharing economic elements.

At present, the users of bean and fruit food are concentrated in super-first-tier cities and first-tier cities, and the economic base is middle class. We can try to use the sharing economy, such as renting picnic tools, kitchen space, and cooking local food in middle school during the trip, which is a good starting point for the lower middle class or the student party.

1. Drainage: Providing venues for domestic online food programs.

There is no doubt that the popularity of "Tip of the Tongue 2" has also ignited bean and fruit food, but because "Tip of the Tongue 2" is a TV program, the age difference of the audience involved will be relatively large. It is a good choice to invest in a well-known domestic food network program for bean and fruit cuisine whose main users are 25-35 years old.

The form of investment is not limited to simple sponsorship, but can be considered to provide a venue to make travel and food together.

2. Drainage and activation: cooperation with local folk markets.

If the number and scale of offline experience stores of Douguo are not yet mature, we can consider cooperating with private markets, such as Beijing’s organic farmers’ market, "Wood Eating Tok", etc., and we can consider gathering e-commerce companies to do offline activities to supplement the modular needs of these centralized users for semi-finished products and gourmet classes.

3. Promotion and retention: LBS positioning function is added to make social interaction high-frequency.

The surrounding modules of the kitchen are crowded with foodies who know their distance, but there may be no clear business model to cut into the social module of the gourmet APP because of lack of organization. You can consider adding labels of personal information, such as personality, food and other habit nodes, starting from personal behavior, so that others can know you better, thus generating social relations.

4. Drainage and promotion: Cooperation with WeChat official account, where domestic foodies gather.

Inviting WeChat official account Big V, a domestic foodie gathering, to cooperate, starting with the content, others provide the content, and we provide the platform and e-commerce entrance to form a mutually beneficial and win-win food ecosystem. At present, there have been some authors of the content of bean and fruit food who have drained it from their personal WeChat official account. If we can cooperate with similar large-scale food, we can make the bean and fruit food have enough traffic entry in WeChat WeChat official account and import it into the bean and fruit food, which will be considered as mutual benefit and win-win.

Specific ways can be achieved by adding "Welcome to join the Douguo Food Community to buy a basket of ingredients and know more about eating" and other graphics and links at the back of WeChat official account Da V’s article, so as to achieve the purpose of drainage.

Further, we can set up an offline activity community centered on gourmet experts, so that the whole community of bean and fruit food can be divided. Users will choose communities based on their preference for eating (the main factor) and their preference for age and education (the secondary factor), which will be conducive to online and offline activity after being divided into small communities.

Author: Turing, a sentimental Internet practitioner, Aspen, WeChat official account: focusing on small emotions for several years.

This article was originally published by @Turing. Everyone is a product manager. Reprinting is prohibited without permission.